Retailer survey: Instead of cutting costs, a focus on smarter investments

Our latest pulse survey reveals that the top priority for retailers is to make their existing investments pay off through more visits.

Dr. Thomas Weinandy

Upside conducts twice-yearly “pulse checks” with retailers like you to better understand business priorities, major challenges, and strategies for growth. Across five waves of this survey, we’ve collected over 7,500 responses and gleaned key insights from your feedback.

When we left things off in Q1 2025, retailers were largely optimistic, but that optimism was tempered a bit by creeping feelings of economic uncertainty. This time around, we saw a continuation of that trend — while also uncovering some new ones.

Overall, these were our key insights:

- Retailers remain confident, though optimism is slowly trending down.

- Cutting costs isn't the priority; making key investments pay off is.

- Loyalty and acquisition are top priorities, but retailers find existing programming isn’t driving behavior change.

- The reported gap between investment and impact is widest for retailers focused on top-of-funnel metrics.

Read on for the full results.

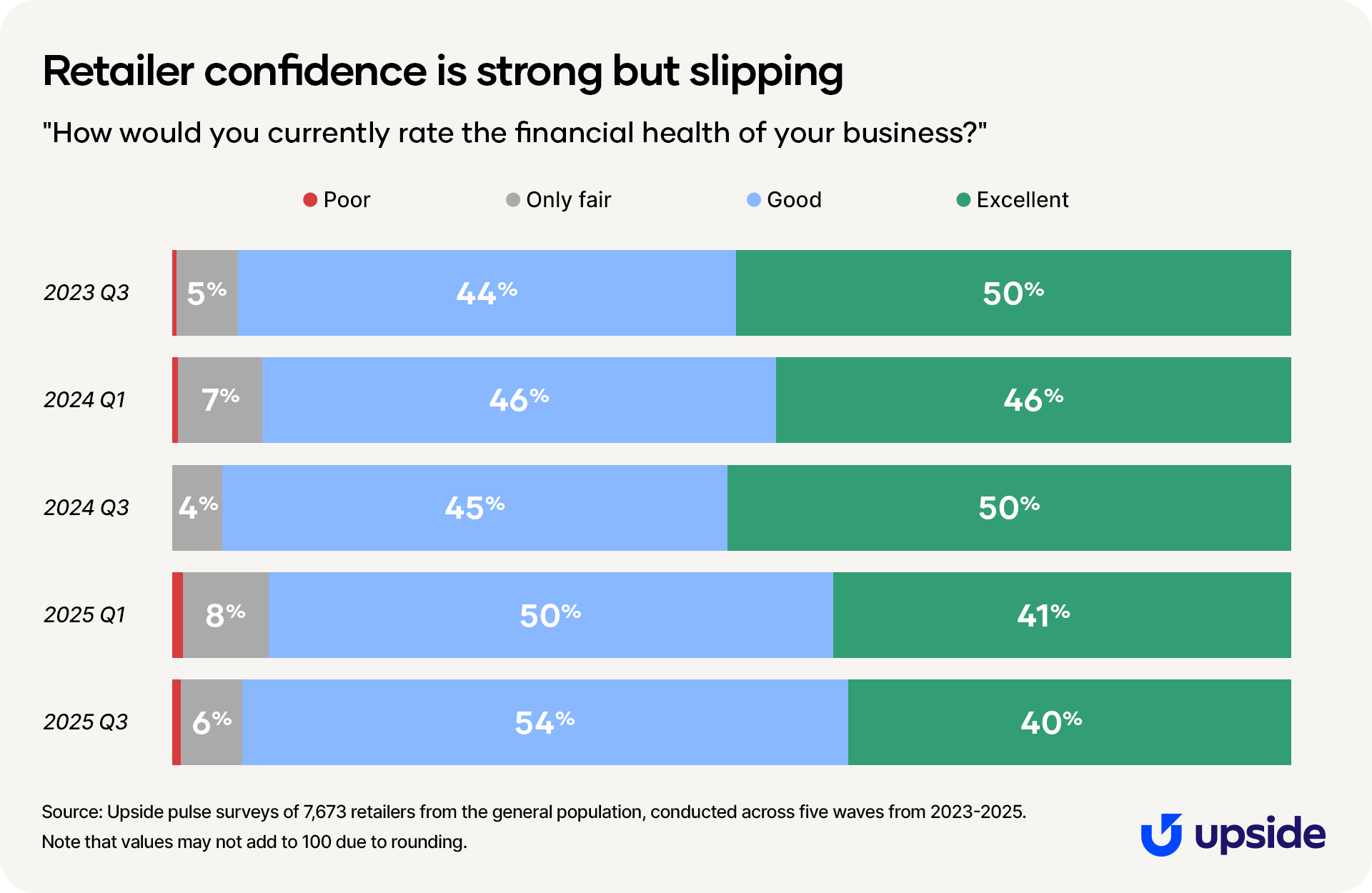

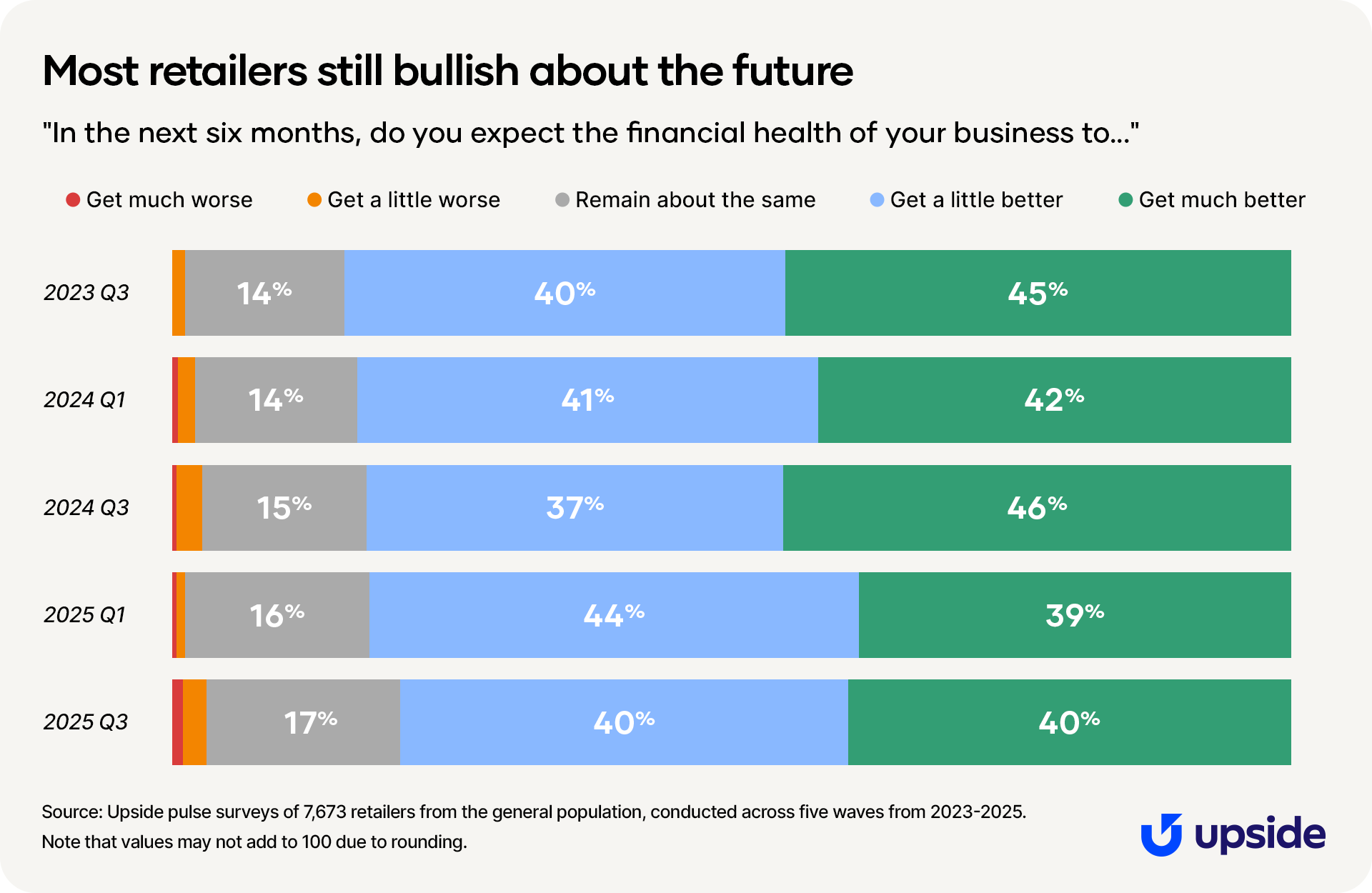

Confident but cautious: Retailers grow slightly more anxious

We begin each survey gauging sentiment — how are you feeling about your financial health today, and how do you think it might change in the next six months?

Overall, retailers are still bullish. Nearly every respondent — 94% — said that their current financial health is either good or excellent. That’s a large and impressive figure.

While that percentage is a three-point improvement over our last survey, we’re seeing that “excellent” responses have been backsliding over the course of 2025. The most common response to this question as recently as Q3 2024, “excellent” responses fell again in this survey, while reports of merely good health have grown. The continuation of this trend through Q3 displays businesses are more conservative or cautious than before.

When it comes to the future, retailers display similar levels of optimism compared to previous years — though for the first time in our survey, the percentage of retailers who expect their financial health to “get much worse” is non-zero. While small, it indicates an uptick in pessimism over previous editions of our survey.

When we break it down by category, we see that fuel and convenience store retailers are slightly more optimistic than the average, and restaurant and grocery retailers are slightly more pessimistic. One reason for the discrepancy could be sustained, elevated margins in the fuel industry.

Less focus on cost-cutting, more on investments that deliver

Retailers are feeling the pressure of rising costs, but rather than tightening their belts, they’re doubling down on making their existing investments deliver more value. Cost-related challenges such as supply chain pressures, labor costs, and inflation continue to rank at the top of their concerns.

But even with these headwinds, most retailers are not looking inward for savings — they’re looking outward for growth. When asked about their top priorities, nearly half of retailers (47%) said they’re focused on driving loyalty and repeat visits, and 45% are focused on acquiring new customers.

Social media has re-emerged as the most popular marketing channel, reversing the decline we observed earlier this year. Other frequently used tactics include websites, online ads, email marketing, and third-party delivery apps.

This shift reflects a clear strategic posture: retailers are trying to grow through volume, not efficiency. They’re placing bets on increasing customer activity rather than pulling back spending. But there’s a catch: The playbook they’ve relied on for years is no longer producing the results it used to. In other words, the impact of this familiar strategy is weakening.

Driving visits is a priority, but the classic playbook is failing

Despite all the investments that retailers have made in recent years, roughly half of retailers report customer behavior has not improved.

- 49% say loyalty program participation (sign ups, usage) has not changed

- 48% say loyal customer behavior (repeat visits, higher spend) has not changed, while another 12% report participation and behavior have actually gotten worse

Why does this matter now?

One reason that it’s particularly relevant could be that retailers made a lot of investments during and following the pandemic. With a bit more time and perspective, they now need those investments to pay off. Otherwise, retailers are not in a position to invest mass amounts of capital elsewhere.

Another potential reason is that digitizing during the pandemic had high ROI with the early adopters winning the most. Now, late adopters have arrived, causing the channels to be oversaturated and less effective than before.

No matter the reason, retailers are saying it’s critical for them to get a return on their investments, but the impact of those investments is dwindling — especially for retailers focusing on driving top-of-funnel metrics.

Digging deeper on the investment-impact gap

Overall, retailers with loyalty programming report that their programs are most effective at achieving top-of-funnel results and least effective at driving bottom-of-funnel results.

Retailers say loyalty programming is less effective at driving bottom-of-funnel results

Retailers say loyalty programs are most effective at gathering valuable customer data — and least effective at driving bottom-of-funnel results.

When asked to rank effectiveness, retailers placed these outcomes in order:

- Gather valuable customer data (most effective)

- Strengthen brand affinity

- Increase new member sign-ups

- Enhance the customer experience

- Increase customer lifetime value

- Increase usage among existing members

In aggregate, it seems like loyalty programs are least effective at the metrics that matter most — or at least the ones that drive profit. Increasing customer lifetime value and increasing usage among existing members both appear towards the bottom of this list. But when we break apart healthy and unhealthy businesses (categorized based on their financial health rating), we actually see a divergence in outcomes.

Healthy businesses are more likely to:

- Grow loyal customer behavior than grow program participation.

- Report they’re better than unhealthy businesses at increasing lifetime value.

Meanwhile, unhealthy businesses are more likely to:

- Grow loyalty program participation than grow loyal customer behavior.

- Report they’re better than healthy businesses at signing up new loyalty program members and increasing program usage.

While 94% of businesses in our sample consider themselves financially healthy, those businesses tend to emphasize metrics that drive behavior change — like visit frequency and spending — over participation metrics like sign-ups. In contrast, less healthy businesses lean more heavily on those participation metrics.

Get more retail data from Upside

Upside analyzes billions of transactions across multiple retail categories and collects tens of thousands of survey responses every year. Browse all our blogs here.

Share this article:

Dr. Thomas Weinandy

Dr. Weinandy is a Principal Research Economist at Upside, providing valuable insights into consumer spending behavior and macroeconomic trends for the fuel, grocery, and restaurant industries. With a Ph.D. in Applied Economics, his academic research is in digital economics and brick-and-mortar retail. He recently wrote a book on leveraging AI for business intelligence.

Similar articles

Request a demo

Request a demo of our platform with no obligation. Our team of industry experts will reach out to learn more about your unique business needs.